Online Store

Online Store

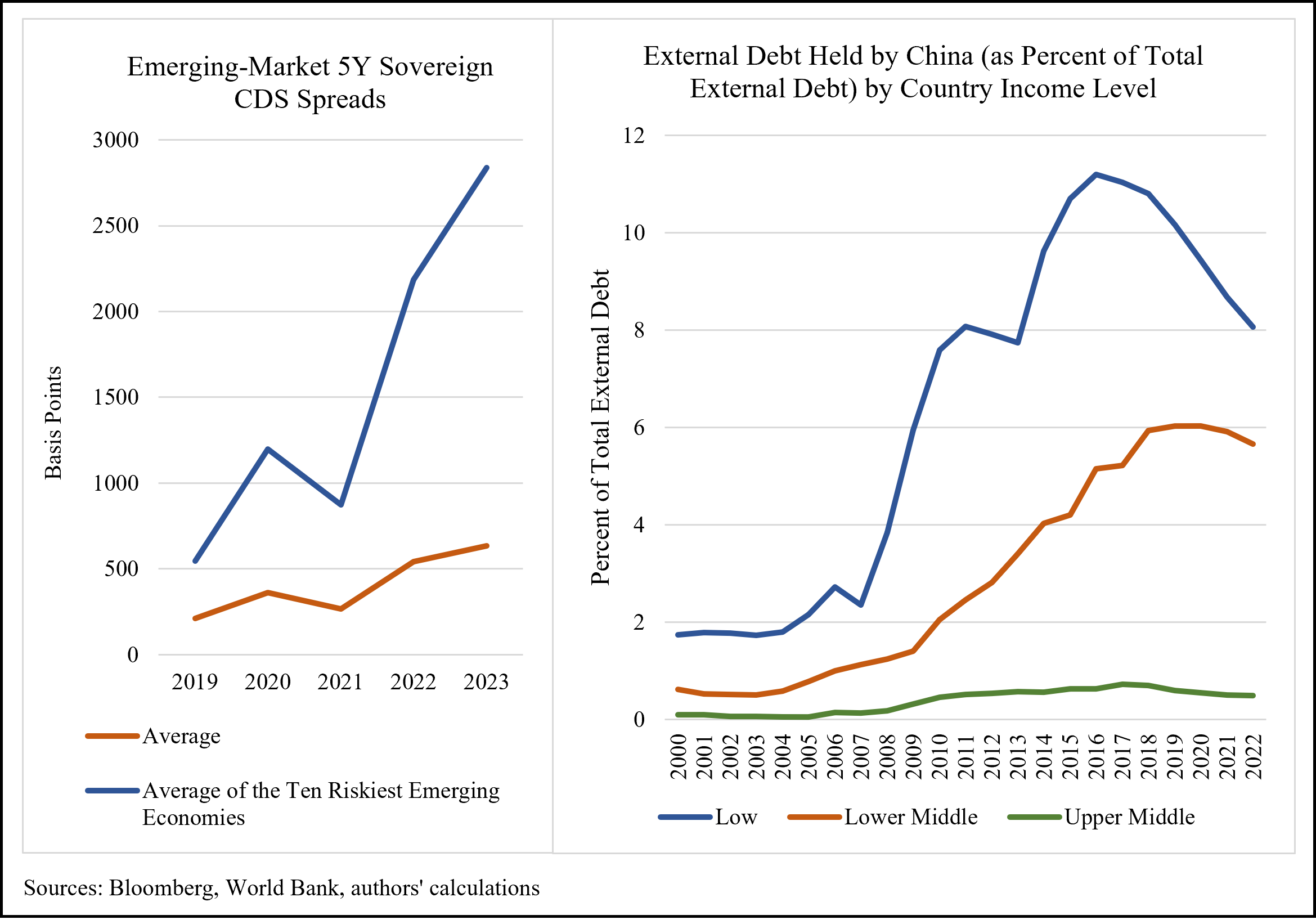

China Has Become a Major Source of Sovereign Default Risk

In our recent column in Barron’s, we argued that the risk of sovereign defaults around the world this year was significant and underappreciated. Our CFR Sovereign Risk Tracker, which we created in 2017, now classifies a record twelve countries as very high risk—meaning that there is at least a 50 percent chance of default within five years. As shown in the left-hand figure above, developing- and emerging-market credit default swap (CDS) spreads—that is, the prices for default insurance—have increased significantly since the beginning of the COVID-19 pandemic.

More on:

In our column, we also argued that politics play an underappreciated role in determining which countries actually default. Increasingly, those politics involve China, whose massive Belt and Road lending initiative, launched in 2013, boosted its position as the dominant creditor to low-income countries—as shown in the right-hand figure above. Though China began scaling back its lending in 2020, it remains the most critical creditor in international negotiations to stabilize the over-indebted nations of Pakistan, Sri Lanka, Ghana, and Zambia. Given China’s steadfast resistance to writing down the debts of its sovereign borrowers, it finds itself in increasing conflict with developed creditor-country members of the Paris Club and International Monetary Fund, who reject having their resources called upon in greater amounts and with greater frequency to bail out Belt and Road “beneficiaries.” We believe that this growing friction will fuel sovereign defaults this year and in years to come.

More on: